Once again national news outlets are reporting that the Canada Revenue Agency has been excoriated by another Auditor General’s Report. This report, it would seem, is the final level of accountability for the bureaucrats who operate the Canada Revenue Agency. While no heads ever roll after a bad report by the AG, bureaucrats do not like being embarrassed or called to the carpet, so there is some hope that some good change could result.

For all the businesses that have felt themselves victims of the Canada Revenue Agency, and there have been many, many cases, the release of a report like this can at least give you some small solace that you are not alone if you have ever had to file an appeal and endure the long wait for a decision. The good news: if you do appeal, there is about a 65% chance you will win your appeal.

In the latest report, the AG finds that the Canada Revenue Agency takes too long to process income tax objections and does not adequately measure its performance results in the handling of those objections. Rather shockingly, what the CRA reported as the time to process an objection was shorter than the actual length of time taxpayers waited because there were steps in the process that the CRA does not count as waiting time.

To avoid paying interest, taxpayers can pay an amount in dispute when they file their objection. Otherwise, they must pay later if their objection is not allowed. With the CRA taking months, even years, to process objections, taxpayers incur higher costs than if the CRA was processing objections efficiently.

If a taxpayer doesn’t pay for an assessment up front, then if their objection is ultimately disallowed, they are required to pay interest of 5% on the disputed amount not paid in advance, and the interest expense is not tax-deductible. But if the objection is ultimately allowed, the taxpayer only gets refund interest at 3%, and it has to be included in income.

In the most recent fiscal year, the waiting period for an objection to be assigned to a worker ranged from three months to over a year. This does not cover the time it takes to actually review the objection and arrive at a decision.

The Canada Revenue Agency’s responded to this by promising to provide taxpayers a more accurate estimate of time to receive a final response to an objection.

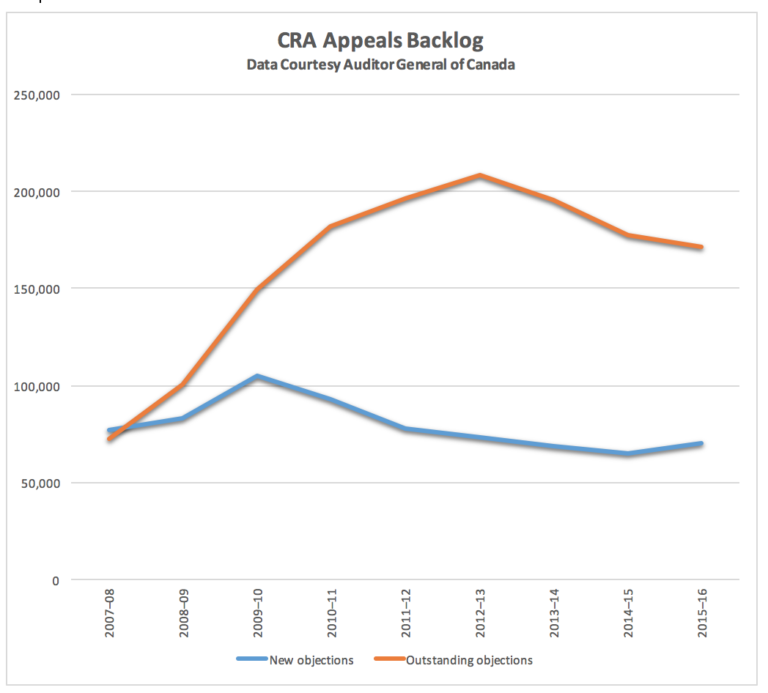

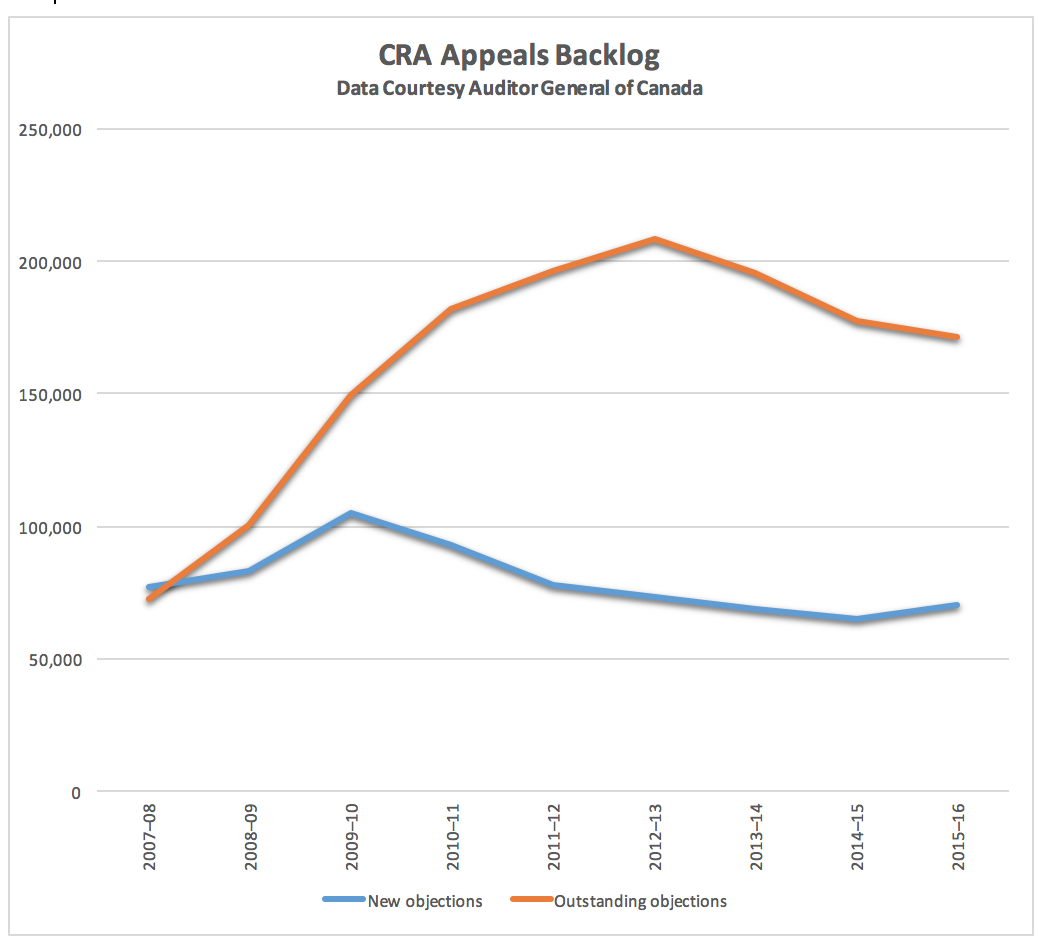

The report then went on to discuss the steady growth of taxpayer objections, noting that over the past 10 years, outstanding income tax objections increased by 171%, while the number of employees dedicated to handling those objections increased 14%.

The AG found that the CRA’s method of measuring timeliness was neither consistent nor complete and did not provide an accurate measure of the time required to process an objection. In addition, CRA was not reporting the actual or average times of taxpayer waits to Parliament, and therefore had no way of determining whether they were meeting their accountability targets. In order to prove it was meeting its timeliness objective, CRA would need to define what timely was. However, the AG found that the Agency no definition or criteria for “timely”, and therefore could not possibly know what would be considered a reasonable amount of time for resolving objections.

Then there was the results of the appeals themselves. The AG found that 65% of objections reviewed resulted in decisions that favoured the taxpayer in full or in part. $6.1 billion taxes out of a total of $11.6 billion in dispute was allowed to taxpayers on Appeal. In that same period, the agency cancelled almost $1.1 billion in related penalties and interest. The accompanying recommendation: “The Canada Revenue Agency should review the reasons objections are decided in favour of taxpayers so that it can identify opportunities to resolve issues before objections are filed.”

The takeaway from this is that there is no feedback loop to auditors whose audits are getting tied up in Appeals, only to be allowed to the taxpayer, and so there is no way for the Agency’s auditors to learn from the mistakes.

As for CRA, they say they are working toward improvements on all of the points put forth, though no specific plans were disclosed. It should be noted that the review did not cover GST/HST.

{kind=link}